Part 3: Your California Climate Disclosure Journey – July 2025 CARB Updates

This third installment in our California Climate Disclosure Journey series builds on Parts 1, “Doing business in CA” explained, and 2, Deadlines & assurance levels to keep you informed on the Climate Corporate Data Accountability Act (SB 253) and the Climate-Related Financial Risk Act (SB 261).

On July 9, 2025, the California Air Resources Board (CARB) released a formal FAQ that gives executives the clearest guidance yet of what CA SB 253 and CA SB 261 will require. CARB confirmed that previously shared reporting deadlines will hold and rules for submitting reports and formatting are to be published later this year.

Circle back to the earlier posts if you need foundational definitions or a roadmap, and read on for an overview of the latest from CARB and next steps for climate compliance.

Latest CARB Updates on California Climate Disclosures

Here are a few common questions clarified in the July 2025 CARB FAQ:

1. Are we in scope for California’s new climate disclosure laws?

CARB is continuing to solicit feedback on definitions for “doing business in California” and revenue thresholds. Presently, a company is considered in scope if it satisfies both of these tests:

- Revenue

- SB 253 – annual total revenue $1 billion or more

- SB 261 – annual total revenue $500 million or more

- Doing business in California

CARB is using the CA Franchise Tax Board (FTB)'s economic-presence tests to determine applicability. If your company revenue meets the SB 253 or SB 261 triggers and you cross any one of these sales, property, or payroll amounts, you must file the required climate disclosures.

- California sales: ≥ $735,019 or 25% of worldwide sales

- California property: ≥ $73,502 or 25% of worldwide property

- California payroll: ≥ $73,502 or 25% of worldwide payroll

2. What must be filed for CA SB 253 & SB 261—and when?

Climate-risk report (SB 261)

- Deadline: January 1, 2026, then biennially

- Format: IFRS S2/TCFD-aligned climate report on FY25/25 data (or FY23/24 data to accommodate first time climate reporters); CARB will provide a docket on December 1, 2025 for public link submissions.

Scope 1-2 greenhouse gas emissions inventory (SB 253)

- Deadline: 2026 (exact date to be set) covering FY25 emissions data

- Assurance: limited in 2026, reasonable from 2030

CARB’s December 2024 Enforcement Notice grants a one-cycle leniency on incomplete Scope 1-2 data if verifiable collection is demonstrated to be under way.

Scope 3 greenhouse gas emissions inventory (SB 253)

- Deadline: 2027 covering FY 2026 emissions data

- Phasing: category coverage may be staggered; assurance begins 2030

3. Consolidation under SB 219

SB 219 would let groups file one parent-level report, streamlining multi-subsidiary structures. CARB is evaluating when foreign parents must consolidate. Legal teams should model both scenarios and be ready to comment on the forthcoming draft rule.

Immediate priorities for executives on CA SB 253 & SB 261

- Run the economic-presence tests for every business entity using FTB thresholds.

- Capture FY 2025 emissions data now; utility meters, fuel logs, refrigerant charges.

- Calculate FY 2025 Scope 1-2 emissions before the year closes; CARB lets companies use “best-available” data for the first 2026 filing if good-faith work is underway.

- Engage an assurance provider this quarter; verifier capacity will tighten rapidly.

- Launch supplier engagement to secure FY 2026 Scope 3 inputs; many sectors see 70%+ of emissions here.

- Draft the climate-risk report and align it to ISSB/TCFD to ensure board approval by Q4 2025 for a January 1, 2026 submission deadline.

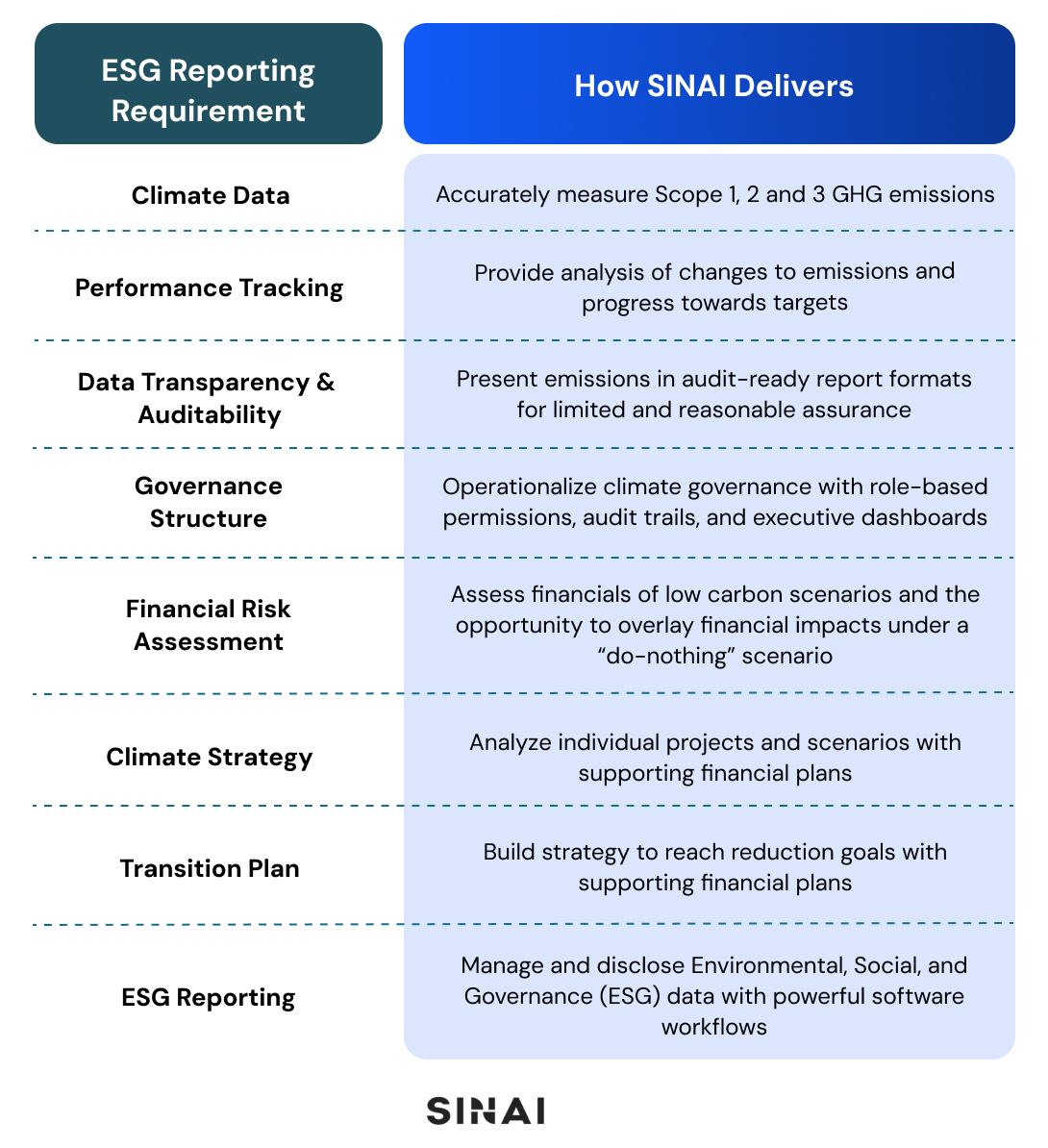

SB 253 & SB 261 Compliance with SINAI

Whether you already rely on SINAI for enterprise-grade emissions management or you’re exploring a platform that covers both decarbonization and ESG regulation, the same AI-driven environment now helps you meet every requirement in California’s SB 253 and SB 261.

Audit-Ready SB 253 Emissions Reporting

Measure and consolidate Scope 1, 2 and 3 data across facilities and suppliers, generate CARB-ready outputs, and package audit evidence for limited assurance in 2026. SINAI’s carbon accounting platform is third-party verified by TÜV Rhineland and aligned with the Greenhouse Gas Protocol, the primary methodology referenced in SB 253 legislation.

- Climate-Risk Analysis for SB 261

Produce an ISSB/TCFD-aligned risk assessment and financial impact modeling, plus a biennial report package for CARB’s 2026 deadline.

- Compliance Automation & Future Coverage

Meet California’s requirements and those of emerging bills in Illinois, New Jersey, New York and Colorado; deadlines, tasks and evidence stay synchronized with the same data that powers your decarbonization strategy.

How SINAI Supports Clients with ESG Reporting

With SINAI, California compliance uses the same trusted data, workflows and AI-driven reporting that power your wider climate program—turning regulatory requirements into strategic advantage.

Ready to see it live? Explore the full solution or connect with a climate expert.

This article is Part 3 of our California Climate Disclosure Journey series. Catch up with Part 1 and Part 2 for foundational guidance on CA SB 253 & SB 261.

.jpg)